You usually capture home financing to have often to purchase property/flat otherwise a block of land for framework regarding property, or recovery, extension and you will fixes for the current home.

While the lender calculates a top eligible count, this is not needed seriously to borrow you to matter

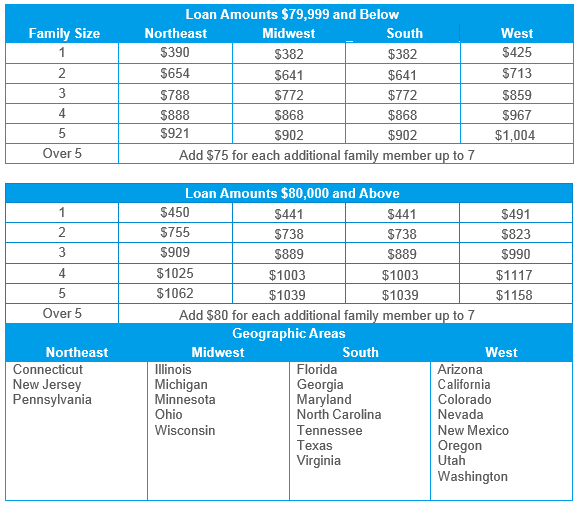

How much financing are We entitled to? Before you start our home loan techniques, determine your own total qualification, that may generally count on the repaying strength. Your own fees capabilities lies in your own monthly throwaway/excess money, and therefore, therefore, lies in factors such as complete month-to-month income/surplus less month-to-month costs, or other circumstances such as spouse's money, property, liabilities, stability of cash, etc.

The lending company needs to make sure it's possible to pay off the loan timely. Generally speaking, a lender takes on you to definitely on the fifty% of your own month-to-month throw away/excess earnings is obtainable to own cost. This new tenure and interest might influence the mortgage matter. Further, financial institutions generally develop a top many years maximum for mortgage individuals, that could effect a person's eligibility.

What is the restriction count I'm able to use? Really loan providers want 10-20% of your own residence's cost once the a down-payment from you. It can be called 'one's own contribution' of the particular loan providers. The others, that is 80-90% of the property worthy of, is actually funded by financial. The total financed count also contains membership, transfer and you will stamp obligations costs.

Actually a lesser matter are going to be lent. One should make an effort to strategy the most out-of down-payment count much less out of home loan so that the focus pricing is remaining during the limited.

The greater the newest month-to-month disposable earnings, the higher will be the amount borrowed you are qualified for

Is a good co-candidate necessary for a mortgage? When someone 's the co-owner of the home in question, it's important he/she even be brand new co-applicant towards mortgage. If you're the actual only real proprietor of the home, people member of their instantaneous family relations will be your co-applicant if you'd like to create.

Just what records are generally sought mortgage recognition? The mortgage application gives a checklist off data getting attached with they, plus an image. As well as the courtroom data connected with the purchase of the house, the bank may also request you to fill in your term and quarters proofs, current salary sneak (validated by boss and you can self-attested from you) and Means sixteen otherwise earnings-taxation go back (having businessmen/self-employed) additionally the past six months bank statements/equilibrium piece, as the applicable. Certain lenders also can wanted collateral safeguards for instance the task off insurance, promise from offers, federal savings certificates, shared financing devices, bank deposits or any other assets.

What is sanctioning and you will disbursement out of financing? Based on the documentary research, the financial institution establishes perhaps the mortgage will be approved or wanted to you. This new quantum of loan that can be approved utilizes which. The bank will give you an effective approve letter stating the loan number, period and interest, certainly most other terms of the house financing. The fresh new mentioned conditions will be valid till the time said inside loans Petrey AL you to page.

If loan is largely handed over to you personally, they amounts in order to disbursement of your loan. This occurs due to the fact financial is with performing technical, judge and you can valuation exercises. One to ount throughout disbursement facing what's mentioned in the sanction letter. During the disbursal phase, you will want to fill in the brand new allocation page, photocopies of title deed, encumbrance certificate as well as the agreement to market papers. The rate into time out of disbursement have a tendency to apply, and never the one as per the sanction page. In cases like this, yet another sanction page gets prepared.